In 2021, Paytm was the talk of the entire country. India’s biggest IPO ever. $2.5 Billion raised in a single day. Vijay Shekhar Sharma on magazine covers. Paytm on every phone, every shop, every street corner.

Today, in May 2026, the story looks very different.

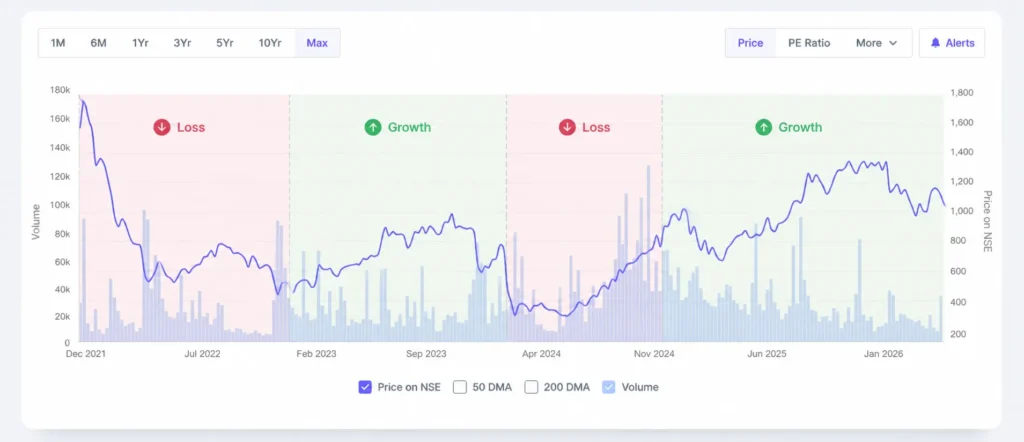

RBI cancelled Paytm Payments Bank’s license on April 24, 2026. The share price has fallen from Rs 2,150 at IPO to around Rs 1,095 today. Market cap has crashed over 50%. And the Payments Bank is being wound up under court supervision.

So what exactly happened to Paytm?

This is not just the story of one company. It is a masterclass in what happens when a startup chases growth without profitability, expands into too many businesses at once, and ignores its regulator one too many times.

Let’s start from the beginning.

Background and Origin Story: A Small Town Boy With a Big Vision

Vijay Shekhar Sharma grew up in Aligarh, Uttar Pradesh — a middle class family, Hindi medium schooling, and a dream to do something big in technology.

He moved to Delhi, studied engineering, and in 1997 started his first company — One97 Communications. The company provided mobile content and value-added services — SMS alerts, ringtones, and mobile internet content. Not glamorous, but it kept the business alive.

In 2010, he launched Paytm — short for Pay Through Mobile. The initial product was simple — mobile recharges and DTH bill payments. Nothing fancy. But deeply useful for millions of Indians who needed an easier way to recharge their phones.

The timing was right. India’s mobile subscriber base was exploding. And Paytm was there to serve them.

What India Looked Like in 2010

In 2010, digital payments were almost non-existent in India. Credit card penetration was tiny. Internet banking was limited to a small urban population. Most Indians paid for everything in cash.

Paytm’s wallet concept — load money once, use it for multiple small payments — was genuinely new for the Indian market. It solved a real problem simply.

But the real rocket fuel came six years later.

The Growth Story: From Mobile Recharges to Everything

2015: Alibaba Changes the Game

For the first five years, Paytm grew steadily but not explosively. Then in 2015, Alibaba — Jack Ma’s Chinese e-commerce giant — invested $680 Million into Paytm.

This was a turning point. With serious capital behind them, Paytm expanded aggressively into e-commerce, launching Paytm Mall to compete with Flipkart and Amazon. They had the wallet. Now they wanted the marketplace too.

2016: Demonetization — The Night Everything Changed

On November 8, 2016, Prime Minister Modi announced the demonetisation of Rs 500 and Rs 1,000 currency notes. Overnight, India’s cash economy froze.

ATM lines stretched for hours. Banks were overwhelmed. People desperately needed a way to pay for everyday things without cash.

Paytm was ready.

App downloads exploded overnight. Vegetable vendors, auto drivers, small shopkeepers — everyone put up a Paytm QR code. People who had never used digital payments learned Paytm in 24 hours out of sheer necessity.

Vijay Shekhar Sharma appeared on the cover of Time magazine. Paytm became a household name across India — from Mumbai apartments to small town markets.

By the end of 2016, Paytm had over 200 Million registered users. It was India’s most downloaded app. Investors were pouring in. The valuation kept climbing.

2017 to 2019: The Super App Dream

After demonetisation, Vijay had a bold vision — make Paytm India’s super app. One app for everything.

So they kept adding. Payments Bank launched in 2017 — Paytm was now officially a bank. Then came Paytm Money for mutual funds and stocks. Then personal loans. Then insurance. Then gold. Then movie tickets. Then travel bookings. Then games.

One after another, without stopping.

The problem? Each new business needed its own team, its own technology, its own marketing, its own regulatory compliance. The focus kept splitting. The losses kept growing.

In 2018, UPI arrived and changed everything again. Google Pay entered India. PhonePe scaled up massively. Suddenly Paytm’s core advantage — its wallet — was becoming less relevant. UPI allowed anyone to pay directly from their bank account without loading a wallet first.

To fight back, Paytm burned massive amounts of cash on cashbacks and discounts to retain users. Revenue could not keep up with spending.

By 2019, Paytm’s annual loss had reached $549 Million. Investors kept the faith because India’s digital payments market was enormous — but the cracks were beginning to show.

2021: India’s Biggest IPO — and Its Most Painful Listing

In November 2021, Paytm went public. They raised $2.5 Billion — the largest IPO in Indian stock market history at that time. The issue price was Rs 2,150 per share.

On the very first day of listing, the stock crashed 27%. It closed at Rs 1,560.

Why? Because institutional investors looked at the numbers carefully for the first time. Paytm was burning enormous cash with no clear path to profitability. The business model was spread too thin. There was no single strong revenue engine.

The IPO that was supposed to be Paytm’s crowning moment became its most embarrassing day.

The Business Model: How Paytm Makes — and Loses — Money

Revenue Streams

Paytm earns money from several sources. Payment processing fees from merchants is their core revenue — every time a business accepts payment through Paytm’s QR code or devices, Paytm earns a small fee. Financial services distribution is their fastest growing line — Paytm partners with banks and NBFCs to distribute loans, insurance, and investment products, earning a commission on each. Their Soundbox and card machine devices sold to merchants generate both hardware revenue and ongoing subscription fees. Commerce and cloud services round out the remaining revenue.

The Profitability Problem

The issue was never that Paytm couldn’t earn money. The issue was that they were spending far more than they earned — on cashbacks, on expanding into new businesses, on building teams for too many verticals simultaneously.

Running a payments business, a bank, an e-commerce platform, a stock broking platform, a lending business, and an insurance platform at the same time requires enormous capital. Each one competed for management attention. None of them reached true scale before the next one was added.

The Role of AI and Technology

Paytm does invest in technology meaningfully. Their fraud detection systems process millions of transactions in real time. Their merchant analytics platform gives small business owners insights into their sales patterns. Their credit underwriting uses AI to assess loan eligibility for customers with no formal credit history — which is genuinely valuable in India where hundreds of millions of people are credit invisible. Their Soundbox device, which announces payment amounts aloud, was a simple but brilliant product designed specifically for Indian merchants who cannot always look at a screen while serving customers.

The technology was often good. The business discipline was the problem.

Key Lessons For Entrepreneurs: What Paytm Teaches Us

Lesson 1: Profitability Is Not Optional

Paytm proved that in India, you can build 200 Million users and still not have a sustainable business. Growth without a path to profit is not a business — it is an experiment funded by investors.

Every entrepreneur needs to be able to answer one simple question at every stage: how does this company make more money than it spends? If the answer is always “later, when we scale” — that is a warning sign.

Lesson 2: Focus Is a Superpower

Paytm tried to be a payment company, a bank, an e-commerce platform, a stock broker, a lender, and an insurance company all at once. Each addition made the others weaker.

The companies that win in India — Zepto in quick commerce, Zerodha in stock broking, PhonePe in UPI payments — win because they are exceptionally focused. They do one thing better than anyone else before moving to the next thing.

Paytm’s biggest competitor PhonePe was a Flipkart spin-off that focused purely on UPI payments for years before expanding. Today PhonePe has a larger UPI market share than Paytm.

Lesson 3: Never Ignore Your Regulator

This is the lesson that ended Paytm Payments Bank.

RBI’s action against Paytm Payments Bank was years in the making — starting with a Rs 5.39 crore fine in October 2023 for KYC and cybersecurity non-compliance, then barring new deposits in January 2024, and finally cancelling the banking licence entirely in April 2026.

This did not happen suddenly. There were warnings. There were fines. There were restrictions. Each one was a signal that went unheeded.

In a regulated industry like banking and financial services, your relationship with the regulator is not a formality. It is the foundation of your entire business. Ignore it, and everything else you have built means nothing.

Challenges and Setbacks: The Troubles Behind the Headlines

The IPO Crash

The November 2021 IPO listing was painful not just for Paytm but for thousands of retail investors who trusted the company’s story. Many bought at Rs 2,150 and watched their investment lose a third of its value in a single day.

This damaged trust in Paytm’s management and raised serious questions about whether the IPO was priced honestly. Critics argued that Paytm knew the business was loss-making and used the IPO to cash out early investors at the expense of public shareholders.

The UPI Competition

When UPI took off in India, it fundamentally weakened Paytm’s core product — the wallet. Paytm adapted by becoming a UPI app itself, but they were now competing with Google Pay, PhonePe, and even WhatsApp Pay on equal footing. The unique advantage they had built was gone.

The RBI Action

On April 24, 2026, RBI cancelled Paytm Payments Bank’s banking licence under the Banking Regulation Act, citing that the bank’s affairs were conducted in a manner detrimental to the interest of the bank and its depositors.

Paytm clarified that the development does not affect its core services — the Paytm app, UPI, Paytm Gold, QR, Soundbox, payment gateway, and other offerings will continue uninterrupted through its partnerships with other regulated banks.

But the reputational damage was enormous. Being the only major fintech in India to have its banking licence cancelled is not a small thing.

The SEBI Issue

Founder Vijay Shekhar Sharma also settled with SEBI over alleged issues with employee stock options, which included a three-year ban on accepting new ESOPs from listed companies and a financial penalty.

This added another layer of regulatory trouble on top of the RBI action and made investors even more nervous about the company’s governance.

Where Are They Now: Paytm in 2026

The picture today is complicated — not dead, but deeply wounded.

Paytm’s share price stands at around Rs 1,095 as of April 30, 2026, with a market cap of approximately Rs 70,143 crore. That is a fall of nearly 50% from the IPO price of Rs 2,150.

Despite the Payments Bank closure, Paytm’s core services — UPI, wallet, Soundbox, payment gateway — continue to operate through partnerships with Axis Bank, HDFC Bank, SBI, and YES Bank.

Analysts at Goldman Sachs maintain a Buy rating on Paytm with a revised target of Rs 1,400, while Jefferies also maintains a Buy, citing intact profitability prospects despite the Payments Bank exit.

Paytm projects a 22% revenue CAGR between FY26 and FY28, with a target of reaching Rs 1,700 crore in net profit and a 16% EBITDA margin by FY28.

So the company is not finished. But it is a very different company from what Vijay Shekhar Sharma once imagined — a full-service financial superpower. That dream is over. What remains is a payments and merchant services business trying to find its footing.

Conclusion: The Real Paytm Lesson

Paytm’s story is one of the most important case studies in Indian startup history — not because it failed completely, but because it had everything and still stumbled badly.

The talent was real. The vision was bold. The timing with demonetisation was perfect. The user base was massive.

But three things undid it — the refusal to prioritise profitability over growth, the inability to focus on doing a few things exceptionally well, and the failure to take regulatory compliance seriously in a heavily regulated industry.

For every entrepreneur building in India today, Paytm is the reminder that how you build matters as much as what you build. A business with 200 Million users and no profit is not a success. It is a warning.

Build focused. Build sustainable. And always, always respect your regulator.

Want to read more Indian startup stories like this? Head over to bizfromzero.com for real breakdowns of how India’s biggest companies were built — and sometimes broken.